A Wellness Spending Account (WSA) is a flexible benefit provided by Canadian employers that reimburses employees for a broad range of wellness expenses beyond traditional group insurance.

These expenses commonly include physical fitness, counselling, family care, and financial wellness contributions. WSA reimbursements are considered taxable benefits, reported on the employee’s T4 slip, and subject to standard payroll deductions, including income tax, CPP, and EI.

The WSA is a cost-effective way for employers to promote a healthy workplace culture while empowering employees to take charge of their well-being in ways that are meaningful to them. Although traditional benefits remain vital, a WSA represents a strategic advancement in recognizing that wellness is individual and extends far beyond conventional medical care.

What is a Wellness Spending Account?

A wellness spending account (WSA) is an employer-sponsored benefit program that provides employees with a set annual allowance to spend on approved wellness expenses of their choice. This flexibility distinguishes a WSA from traditional group benefits, in which the insurer and employer define coverage categories with little room for personal preference.

A WSA works on a straightforward model: the employer funds the account, the employee pays for an eligible expense out of pocket, submits a receipt through the employer’s benefits platform or a third-party administrator, and receives a taxable reimbursement.

The essential advantage of this structure is that it places control over expenditures in the employer’s hands while still allowing employees to tailor their wellness support to their personal needs and lifestyle. Employers can incentivize wellness while capping costs through pre-defined limits.

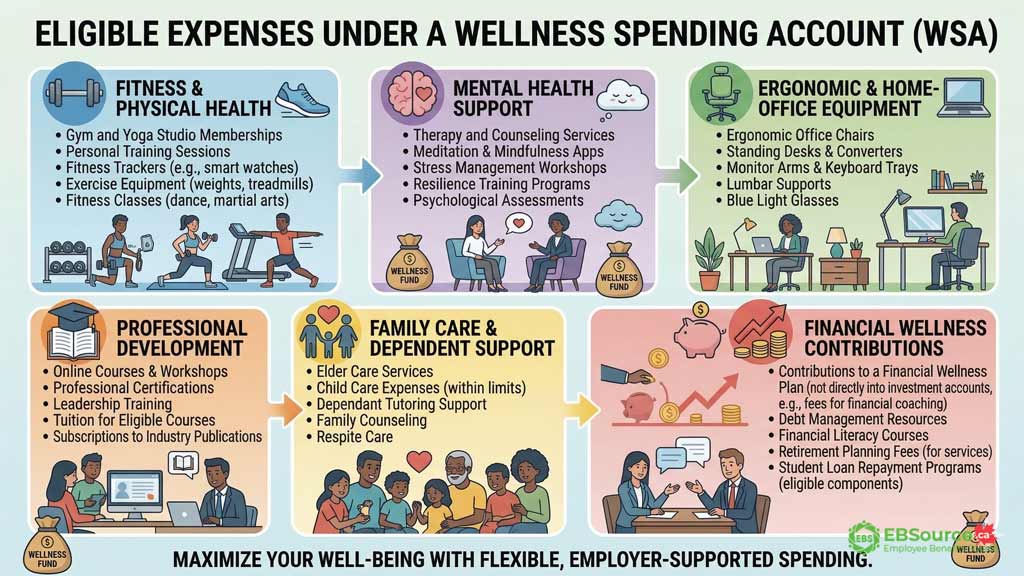

What are Eligible Expenses Under a Wellness Spending Account?

Depending on the provider and plan design, a WSA may cover various categories, generally including physical fitness, mental health, nutrition, personal development, and family care.

Here are some specific examples of items that can be covered:

Fitness and Physical Health

- Gym and fitness class memberships

- Personal training fees

- Fitness equipment (yoga mats, weights, treadmills, ellipticals, stationary bikes, etc.)

- Fitness gear and accessories (workout clothes, running shoes, activity trackers, etc.)

- Race registration fees

- League sports fees

- Ski passes

- Bike shares

Mental Health

- Counselling copays

- Relationship counselling

- Addiction counseling

- Meditation and mindfulness classes

Nutrition

- Weight loss programs/apps

- Nutritional supplements

- Nutrition classes and counselling

- Meal delivery programs

- Hydration products (water bottles, filters, etc.)

Personal Development

- Meditation and mindfulness apps

- Meditation and yoga retreats

- Stress management classes

- Professional development courses

- Professional development conferences/events

- Life Coaching

- Financial well-being apps

Family Care

- Child care

- Elder care

- Caregiver support programs

- Pet care services or insurance

Because WSA expense lists are not regulated by the CRA, the specific items available to you always depend on which categories your employer has activated in the plan document. These examples should be treated as plan-specific, not universal.

Always check your benefits provider’s online portal or contact your plan administrator to confirm which categories and specific items are included in your plan before you make a purchase.

Expenses Commonly Excluded From WSAs

WSA plans commonly exclude CRA-approved medical expenses, health insurance premiums, and items unrelated to wellness. Any expense eligible for tax-free reimbursement under a Health Spending Account (HSA) is generally ineligible for a WSA.

Some examples of commonly excluded items are:

- Prescription medications are only eligible under a Health Spending Account. Dental and vision care, including cleanings, fillings, and eye exams, similarly belong in the HSA stream.

- Chiropractic treatments are considered medical and thus not WSA-eligible. Massage therapy may also fall outside WSA eligibility unless the employer explicitly frames it as a general wellness service.

- Health insurance premiums cannot be reimbursed through a WSA. Over-the-counter medical supplies, including bandages and pain relief products, are also typically excluded.

- Medical equipment and devices such as hearing aids, CPAP machines, and crutches are CRA-eligible medical items and therefore belong in the HSA.

- Expenses unrelated to wellness, such as alcohol, tobacco, and general entertainment, are universally excluded from WSA plans.

If your employer offers both an HSA and a WSA, the correct approach is to route CRA-eligible medical costs to the HSA first, then use the WSA for non-medical wellness items.

Are Wellness Spending Accounts Taxable?

Yes, wellness spending accounts represent a taxable benefit to employees because they cover non-medical wellness items that do not meet strict medical criteria. This means that any amount allocated to an employee through a WSA is added to their T4 income and subject to standard payroll deductions (income tax, CPP, and EI).

However, the employer contributions to fund the master WSA account remain tax-deductible as a business expense. Any unused plan-year-end funds that are forfeited back to the employer are non-taxable.

The taxability of reimbursements is taken into account during WSA setup. Limits and allowances can be higher than with an HSA, since any funds used will be taxed.

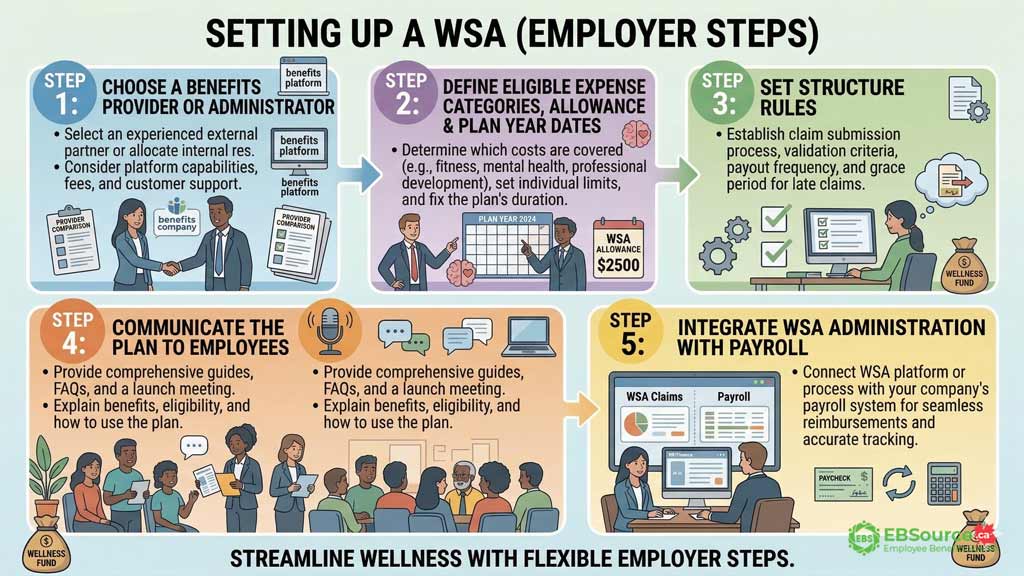

How to Set Up a Wellness Spending Account

The process of establishing a wellness spending account is relatively straightforward: from partnering with a WSA provider to setting an allowance, defining structure rules, communicating the plan, and integrating WSA administration with payroll for taxable-benefit reporting.

Here is how the setup process works in detail:

- Select a Provider: Research and choose a WSA provider. This could be a major insurance carrier, such as Sun Life or Canada Life, or a specialized third-party administrator, such as Olympia Benefits, myHSA, or Wello. When evaluating providers, consider their platform’s ease of use, claim processing times, administrative fees, and reporting capabilities.

- Define Your Goals & Budget: Determine what you want to achieve with the program (e.g., improve fitness, support mental health) and set a realistic budget for employee allowances.

- Design the Plan: Decide on eligibility (e.g., full-time employees only, waiting periods), the list of covered expense categories, and the annual allowance amount.

- Communicate to Employees: A successful launch depends on clear communication. Educate your team on how the WSA works, what’s covered, how to submit claims, and the tax implications.

- Launch and Monitor: Fund the account and launch the program. Use the provider’s analytics to monitor utilization rates and see which categories are most popular, allowing you to refine the program over time.

On the employee side, the enrollment process typically entails:

- Acknowledge receipt and understanding of the coverage options.

- Log in to the online portal or app to submit claims and view the balance.

- Use the provided payment card linked to WSA for easy payments (if offered).

Ongoing tasks for employees are submitting claims, monitoring balances, and ensuring expenditures adhere to guidelines.

How Much Does a Wellness Spending Account Cost?

The cost of implementing a WSA is borne by the employer’s contribution to the master account. This will vary based on employer size, the funding amount per employee, the percentage of employees expected to use the account, and the number of years employees can accumulate balances.

Some factors that influence WSA pricing:

- Employer Size: Accounts with 500+ employees often have lower administrative fees.

- Funding Amount: The dollars allocated per employee.

- Utilization Rate: The percentage of employees expected to use the WSA.

- Plan Design: The eligibility period, rollover allowance, and forfeiture rules.

- Administrative Fees: Charged by the vendor to manage the account.

For example, a company with 75 employees offers a $300 WSA to all staff. If they anticipate 50% utilization and the vendor charges a $3 per employee per month admin fee, the annual cost would be:

- 75 employees x $300 per employee funding amount = $22,500

- $22,500 total funding amount + ($3 per employee per month x 12 months x 75 employees) $2,700 admin fee = $25,200 total annual cost

Employers can receive quotes specific to their plan design parameters to determine precise pricing.

WSA vs. HSA: What Are the Key Differences?

While both WSAs and HSAs provide employees with personalized spending funds, they serve distinct purposes, each with different tax treatment, regulatory oversight, and eligible expense categories.

The following comparison highlights the core structural differences between a WSA and an HSA:

| Feature | Wellness Spending Account (WSA) | Health Spending Account (HSA) |

| Tax Status | Taxable benefit to the employee. | Non-taxable benefit to the employee. |

| Eligible Expenses | Defined by the employer. Covers a broad range of wellness and lifestyle items. | Defined by the CRA under the Income Tax Act. Limited to eligible medical and dental expenses. |

| Primary Purpose | To promote general well-being, lifestyle improvements, and employee perks. | To cover out-of-pocket medical costs not covered by provincial or group insurance plans. |

| Rollover of Funds | Generally, unused funds are forfeited at year-end and returned to the employer. | Can often be rolled forward for at least one year, depending on the plan design. |

Wellness Spending Accounts are considered a taxable benefit by the Canada Revenue Agency. HSAs, by contrast, are generally structured as a Private Health Services Plan (PHSP), so benefits received from the plan are non-taxable. If PHSP conditions are met, an employee can enjoy the benefits without declaring them on their income tax return.

Many employers in Canada offer both health and wellness spending accounts to their employees. Offering both enables employees to tailor their benefits to their lifestyles, while companies can attract top talent with a more flexible, adaptable plan. If your organization is considering this structure, the key is to communicate clearly which account covers which expenses, so employees submit claims to the correct account and avoid unnecessary tax consequences.

WSA vs. PSA: Is There a Difference?

No, there is no functional difference between Personal Spending Accounts (PSAs) and Wellness Spending Accounts. The distinction is based on the naming conventions used by different insurance carriers and third-party administrators. Some providers prefer the term “Wellness Spending Account” to emphasize health and well-being, while others use “Personal Spending Account” to highlight the highly customized, flexible nature of the benefit.

Regardless of the name, they all operate under the exact same Canada Revenue Agency (CRA) guidelines. The CRA tax rules, the broad categories of eligible lifestyle expenses (such as fitness, mental health, and personal development), and the setup processes apply equally to both.

Is a Wellness Spending Account Right for Your Business?

On the employer side, a WSA may be a good fit for those who want more flexible wellness support and can manage the related payroll and plan administration rules.

The critical considerations for employers evaluating whether to offer a WSA include:

- Budget – What amount can reasonably be allocated towards wellness incentives annually?

- Company Culture – Does promoting health align with the company’s mission and values?

- Benefits Strategy – Does the existing benefits plan leave gaps that a WSA could help fill?

As long as the program aligns with corporate goals, any employer committed to employee well-being can effectively leverage a WSA, regardless of company size.

Employees will have access to the WSA if they meet the eligibility criteria outlined by their employer. Most accounts extend eligibility to all employees, but employers can also implement service-based requirements. For example, employees may need to be with the company for six months before accessing the WSA funds.