Choosing the right deductible for a small business health plan is a straightforward process. It begins with selecting the best deductible structure for your team, then moves on to evaluating key factors to determine the ideal amount. The process concludes with confirming your final plan design with the insurance provider.

Understanding how to choose the right deductibles is one of the most influential decisions an SME employer makes when designing a group health benefits plan, as it can directly affect monthly premiums, employee out-of-pocket costs, and the overall value of the benefits package. Let’s explore each of these stages in detail below.

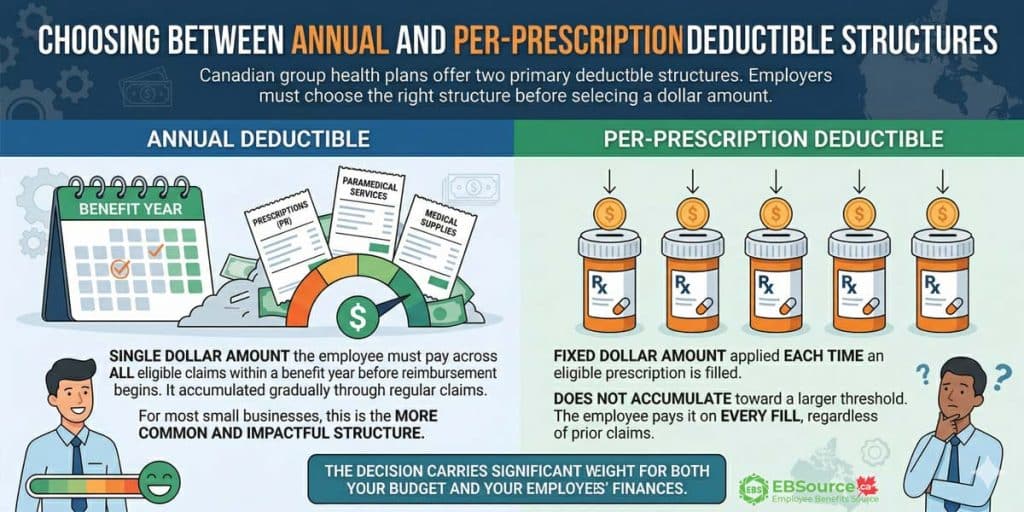

Choosing Between Annual and Per-Prescription Deductible Structures

Canadian group health plans offer several deductible structures, with two of the most common being annual and per-prescription. However, since plans can apply deductibles differently across benefit categories or even combine structures, the employer must choose the right one before selecting a dollar amount.

Let’s break down the two main options you’ll see in Canadian group plans:

Annual deductible

This is a single dollar amount the employee must pay across all eligible claims within a benefit year before the insurer begins reimbursing.

The amount accumulates gradually through regular claims, and different claim types, including prescriptions, paramedical services, and medical supplies, can all count toward satisfying it.

Per-prescription deductible

This is a fixed dollar amount applied each time the employee fills an eligible prescription. Unlike the annual deductible, it does not accumulate toward a larger threshold; the employee pays it on every fill, regardless of how many prescriptions have already been claimed.

That said, for most small businesses, the annual deductible is the more common and impactful structure. The decision on its dollar amount carries significant weight for both your budget and your employees’ finances.

Once you’ve chosen the structure, you can then move on to determining the right dollar amount for your plan.

Source: https://www.bbd.ca/blog/group-insurance-deductible/

What Are the Key Factors for Choosing the Right Deductible Level?

Employers should evaluate five key factors: workforce demographics, annual benefits budget, expected claims patterns, employee retention priorities, and plan renewal dynamics when selecting a deductible amount.

The right decision comes from carefully considering these competing needs to find the best fit for your specific company:

Workforce demographics

The age, health profile, and occupational risk of the employee group shape how much out-of-pocket cost employees can reasonably absorb. Consider the following common scenarios:

- A younger, generally healthy workforce may not require frequent medical care and could be comfortable with a higher-deductible plan in exchange for lower monthly premiums.

- An older, more experienced workforce, or employees with families, may have more consistent healthcare needs. For them, a lower deductible provides greater peace of mind and more predictable out-of-pocket costs when they access care.

- Similarly, employees in physically demanding or higher-risk jobs may benefit from a lower deductible, as it reduces the financial barrier to treating potential injuries.

Annual benefits budget

Every benefits decision is constrained by the company’s overall budget. The deductible you choose has a direct impact on your monthly insurance premiums.

A higher deductible generally results in lower premium costs, and those savings can be redirected to broader coverage categories, such as adding paramedical, mental health, or vision benefits.

For companies on a tight budget, this trade-off may be the only way to maintain breadth of coverage without raising the employer’s total cost.

On the other hand, a lower deductible means the insurance plan starts paying for services sooner, but this comes with a higher monthly premium.

That said, some employers choose to offer multiple plan options, such as a high-deductible plan paired with a Health Savings Account (HSA) and a more traditional low-deductible plan. This allows employees to select the option that best fits their personal financial situation and healthcare needs.

Expected claims volume

Prior-year claims data, or industry benchmarks for a new plan, can help predict how often employees will reach the deductible threshold.

By analyzing these data, you can better forecast how often your employees are likely to use their health benefits. Then, you can make a more informed decision:

- If your team has a history of high utilization (frequent doctor visits, prescriptions, etc.), a lower deductible can lead to greater employee satisfaction, as they will see the value of their plan more quickly.

- If your workforce has historically low medical needs, a higher deductible can be a smart financial choice. It lowers premium costs for everyone without significantly impacting most employees, who may not have enough medical expenses to meet the deductible anyway.

Employee retention and recruitment

In a competitive job market, a strong employee benefits package is a powerful tool for attracting and keeping valuable employees.

The deductible is one of the most visible parts of a health plan, and a lower deductible often signals to potential and current employees that the company is invested in their health and financial security. For an SME competing for talent against larger corporations, a generous health plan can be a key differentiator that helps level the playing field.

Plan renewal dynamics

To manage long-term costs, it’s crucial to understand how your insurance provider will calculate your premiums at your annual renewal. This process often depends on the size of your company, as small and larger businesses are usually priced differently:

- For Small Businesses (Pooled Plans): Insurers typically group small companies together and base renewal rates on the entire pool’s claims. This approach provides stability and protects your business from a sharp premium increase, even if your team has a year with high medical claims.

- For Larger Businesses (Experience-Rated Plans): Your renewal premium is directly tied to your own employees’ claims history. A year with high medical costs will likely lead to a higher premium. In this case, choosing a higher deductible can be a direct strategy to help control future rate increases. (Source)

To make your decision clearer, the table below distinguishes between pooled plans and experience-rated plans, as they differ in premium calculation, renewal risk, and deductible strategy:

| Feature | Pooled Plans | Experience-Rated Plans |

| Best For | Small Businesses (typically under 25-50 employees) | Larger Businesses |

| Premium Calculation | Premiums are based on the combined claims history of a large pool of similar small companies. | Premiums are based directly on your own company’s claims history from the previous year. |

| Renewal Risk | Low and predictable. A high-claim year for your team will not cause a sharp rate increase because the risk is spread across the entire pool. | High and variable. A high-claim year will likely lead to a significant premium increase at renewal. A low-claim year may lead to a smaller increase or stable rates. |

| Deductible Strategy | A deductible helps manage the overall cost of the plan within the pool. | A higher deductible can be used as a direct strategy to control your company’s claims costs and mitigate the risk of large renewal increases. |

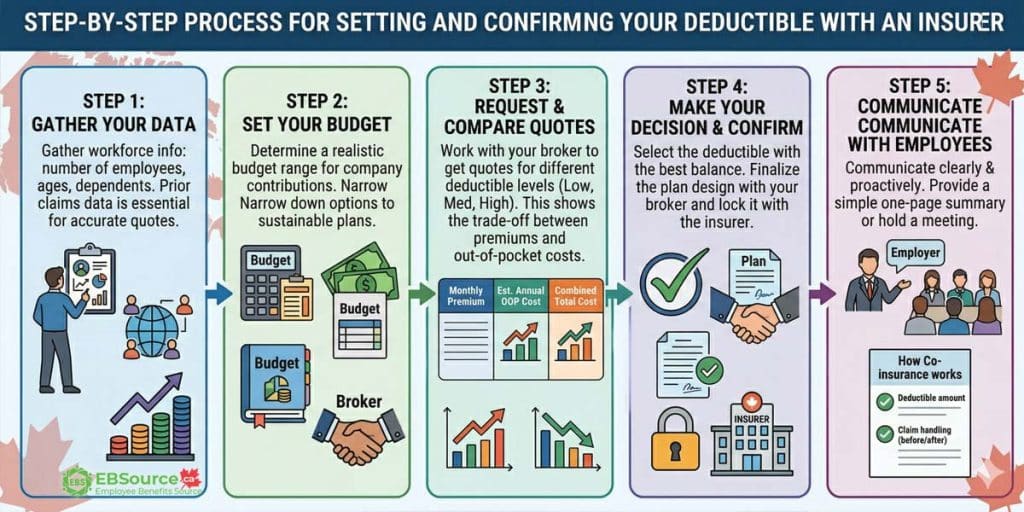

Step-by-Step Process for Setting and Confirming Your Deductible With an Insurer

The practical process involves gathering data, setting your budget, comparing options, and communicating your decision effectively to your team.

Once the employer has evaluated the five factors above and identified a target deductible range, the following steps move the decision from analysis to a confirmed plan design.

Follow the five steps to move from evaluation to a confirmed deductible level:

Step 1: Gather Your Data

Gather key information about your workforce, including the total number of employees, their ages, and how many have dependents.

Your prior claims data will also be useful if you have an existing plan, as this information is essential for insurers to provide accurate quotes.

Step 2: Set Your Budget

Determine a realistic budget range for your company’s contribution to health insurance premiums. This will help you and your broker narrow down the options and focus on plans that are financially sustainable for your business.

Step 3: Request and Compare Quotes

Work with your broker to get quotes from insurers at several different deductible levels (e.g., a low, medium, and high option).

This is the most critical part of the process, as it allows you to see the direct trade-off between premium costs and your employees’ out-of-pocket expenses.

When you receive the quotes, ask your broker to create a simple side-by-side comparison that shows:

- The monthly premium for each option.

- The estimated annual out-of-pocket cost for an employee, based on average use.

- The combined total cost (premium + employee out-of-pocket).

For example, consider a 10-employee team with an average age of 29 and a monthly benefits budget of $1,500. The table below shows the kind of quotes they might compare, making it easy to see how the deductible directly impacts both the company’s premium and the employee’s out-of-pocket costs.

| Feature | Option A (Low Deductible) | Option B (Balanced) | Option C (High Deductible) |

| Annual Deductible | $25 per person | $50 per person | $100 per person |

| Co-insurance | 80% | 80% | 80% |

| Total Monthly Premium | $1,150 | $1,050 | $940 |

| Total Annual Employer Cost | $13,800 | $12,600 | $11,280 |

| Employee OOP (with $500 in claims) | $120 ($25 + 20% of $475) | $140 ($50 + 20% of $450) | $180 ($100 + 20% of $400) |

Important note: This table is for illustrative purposes only; actual quotes will vary based on your insurer, employee demographics, location, and claims history.

This kind of comparison will help you identify the point where the premium savings from a higher deductible no longer justify the additional financial risk for your employees.

It’s also important to note how other plan features, like co-insurance and plan maximums, may change between the different tiers, as these also impact the total cost.

To better understand how these elements work and when to use each approach, see our guide on co-insurance vs. co-pay.

Step 4: Make Your Decision and Confirm

After evaluating the options, select the deductible that offers the best balance for your company and your team. Once you’ve made your choice, you’ll work with your broker to finalize the plan design and lock it in with the insurer.

Step 5: Communicate with Your Employees

A well-chosen plan can still lead to confusion and frustration if employees don’t understand how it works. So, you need to communicate your decision clearly and proactively. Provide a simple, one-page summary or hold a brief meeting to explain:

- How co-insurance works and what an employee can expect to pay out-of-pocket.

- What the deductible is and how much it is.

- How claims are handled before and after the deductible is met.

How Does Tax Treatment Support the Deductible Decision?

Tax treatment is another important factor when setting deductibles because it affects both employer costs and employee value. However, it’s important to clarify that the deductible amount itself does not determine a plan’s tax status. Eligibility for tax benefits is based on the types of expenses the plan covers.

In most provinces, the premiums a company pays for health and dental coverage are considered a tax-deductible business expense, while for employees, they are a non-taxable benefit. This is possible when the plan qualifies as a Private Health Services Plan (PHSP) under the rules of the Canada Revenue Agency (CRA). The CRA clearly states that medical expenses paid out under a PHSP are not taxable to the employee. (Source)

This tax-efficient structure is one of the reasons group health plans offer such great value: employers can deduct the cost, while employees typically receive their reimbursements tax-free.

Health Care Spending Accounts (HCSAs), which are usually set up under PHSP rules, can further support deductible decisions. They allow employers to combine a core insurance plan with flexible reimbursement funds for their staff. HCSA reimbursements are generally given to employees on a tax-free basis. However, Quebec is an important exception. There, this benefit is considered taxable for provincial income tax purposes. (Source)

For small businesses, this tax treatment often supports the use of moderate deductibles paired with employer-funded spending accounts, which help control premiums while preserving perceived employee value.

Because tax rules can affect the true after-tax cost of your plan, it’s always best to confirm the PHSP eligibility requirements, which are based on the types of expenses covered, not the deductible amount, and any province-specific tax rules with your insurer or tax advisor before you finalize your deductible levels.

Frequently Asked Questions When Setting Deductibles for SME Health Plans in Canada

[rank_math_rich_snippet id=”s-c8b89e1c-34bb-43e2-8229-1cda03a7c423″]