The CPP retirement pension is a monthly benefit paid to eligible Canadians who contributed to the Canada Pension Plan (CPP) during their working years. You qualify for this pension if you are at least 60 years old and have made at least one valid CPP contribution.

The amount you receive depends on your earnings history, how long you contributed, and the age at which you choose to start. That starting age, which can fall in any month between 60 and 70, permanently adjusts your monthly amount, and is the single most significant variable in your CPP calculation.

Understanding how the CPP retirement pension works is a critical part of retirement planning, as the decisions you make, especially about when to start collecting, can have a permanent impact on your monthly income for decades to come.

What is the CPP Retirement Pension?

The CPP retirement pension is a monthly, taxable benefit designed to replace a portion of your income in retirement.

The CPP retirement pension is not an employer-provided benefit. Instead, it is an earnings-related, contribution-funded program administered by Service Canada on behalf of the federal government. You and your employers contribute a portion of income on a paycheque basis, up to a yearly maximum. These contributions are pooled together and invested to grow over time.

When you retire, you get a monthly payment for life regardless of how long you live, provided you meet the eligibility requirements. This serves as a reliable financial safety net, helping maintain your standard of living during retirement.

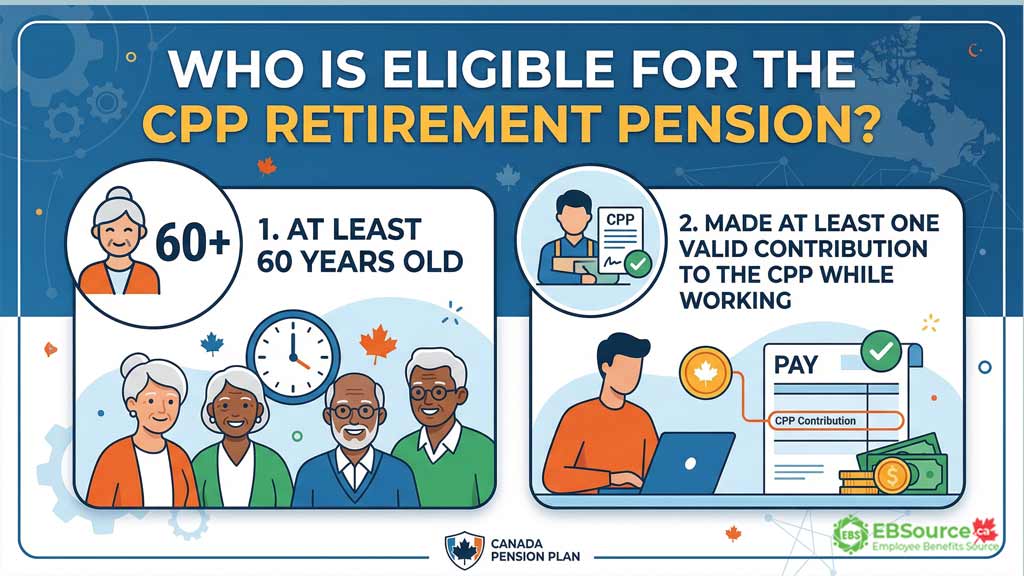

Who is Eligible to Receive the CPP Retirement Pension?

Qualifying for this pension is straightforward: you must be at least 60 years old and have made at least one valid contribution to the CPP while working.

A valid CPP contribution is any contribution made on earnings from employment or self-employment in Canada that exceeded the Year’s Basic Exemption ($3,500) and fell at or below the Year’s Maximum Pensionable Earnings ($74,600 in 2026, as announced by the CRA), or from CPP credits you received after a divorce or separation (credit splitting).

Note: CPP applies in every province/territory except Québec, where the QPP applies. If you worked in both Quebec and another province/territory, CPP and QPP work together, but you may need to follow Quebec-specific steps.

You can begin receiving your CPP retirement pension at age 60, regardless of your current employment status. Whether you are working full-time, part-time, or are self-employed, your employment income will not reduce or cancel your pension payments.

One thing Canadians often overlook is that CPP does not start automatically. You must submit an application to begin receiving CPP payments. It is recommended to apply in advance so you can start receiving CPP on time.

Important note: The CPP applies across Canada, except in Quebec, where the Quebec Pension Plan (QPP) applies. If you worked in both Quebec and another province/territory, CPP and QPP work together, but you may need to follow Quebec-specific steps.

How Much CPP Retirement Pension Could You Receive?

The amount of your CPP pension depends on three main factors: your average earnings throughout your working life, how long you contributed to the CPP, and the age you decide to start your pension. In addition, to ensure life’s interruptions do not unfairly lower your pension, Service Canada applies specific dropout provisions that exclude periods of low or no income from your final calculation.

Below is how each factor affects your personal benefit amount:

Average Lifetime Earnings

The CPP will assess how much you earned over your entire career. They compare your earnings to the Yearly Maximum Pensionable Earnings (YMPE), which is the yearly maximum amount on which you make CPP contributions. If your salary exceeds the YMPE, only the portion up to the maximum is used to calculate your pension.

Number of Contribution Years

The number of years you were making valid CPP contributions has a major impact. Generally, the more years you contributed, the higher your monthly pension.

Starting Age

If you take your CPP pension before age 65, the amount is reduced. If you delay your pension start beyond age 65, your benefit increases. The adjustment factor depends on your specific birthdate.

Dropout Provisions

To boost your final pension amount, Service Canada automatically excludes certain low-earning periods from your calculation. The general dropout provision automatically excludes up to 8 years of your lowest-income months, compensating for periods when your income was relatively low.

The child-rearing provision protects parents by excluding months where earnings dropped because they were caring for a child under age 7. Additionally, the disability dropout covers months when you received a CPP disability pension, protecting your retirement pension amount.

2026 CPP Retirement Pension Amounts: Maximum vs. Average

For the 2026 benefit year, the maximum monthly CPP retirement pension for someone starting at age 65 is approximately $1,507.65. This amount applies only to individuals who have contributed at or above the maximum pensionable earnings level for most of their working life.

Actual personal CPP payments are usually lower. According to the latest published data, the average monthly CPP for new beneficiaries at age 65 is $925.35. These figures are updated annually by the Government of Canada and reflect recent contribution data.

The significant gap between the maximum and average figures exists because receiving the maximum pension requires having contributed at or near the maximum earnings limit for most of your career. Most Canadians have years with lower earnings, time out of the workforce, or periods of self-employment, which result in a pension amount closer to the average.

Therefore, you should not assume you will receive the maximum amount. The most accurate way to see CPP estimates tied to your record is My Service Canada Account (MSCA), where you can view benefit estimates and your statement of contributions. You can also use the official Canadian Retirement Pension Calculator to combine your CPP estimate with other income sources (like OAS, workplace pensions, RRSP/RRIF) for retirement planning.

Source: How much you could receive – Canada.ca

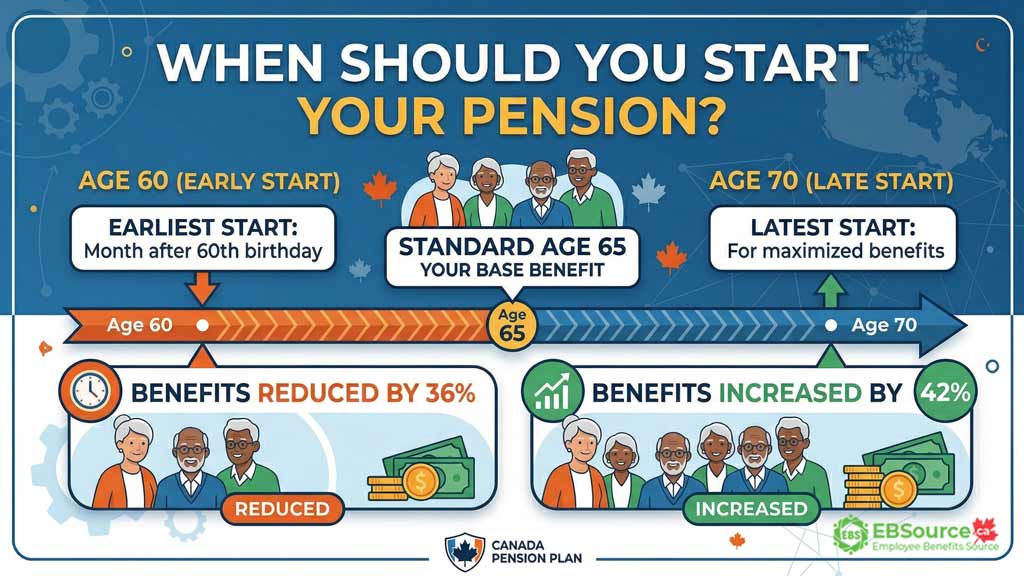

When Should You Start Your Pension?

One decision that has a major impact on your CPP retirement pension is choosing when you take your first payment. The age you choose permanently changes your monthly payment amount.

You have some flexibility in starting to receive your CPP as early as age 60 or as late as age 70. The standard age is 65; however, your CPP retirement pension can start as early as the month after your 60th birthday. This will reduce benefits by 36%, while waiting until 70 increases them by 42%.

The table below shows how the CPP payment is adjusted by age:

| Age to Start CPP | Adjustment Rate | Example: Base $1,000/month |

| 60 | -36% | $640 |

| 61 | -28.8% | $712 |

| 62 | -21.6% | $784 |

| 63 | -14.4% | $856 |

| 64 | -7.2% | $928 |

| 65 | 0% | $1,000 |

| 66 | +8.4% | $1,084 |

| 67 | +16.8% | $1,168 |

| 68 | +25.2% | $1,252 |

| 69 | +33.6% | $1,336 |

| 70 | +42% | $1,420 |

CPP Payment Adjustments by Age

Source: When to start your retirement pension – Canada.ca

You should consider your complete retirement income picture before deciding when to take your CPP retirement pension. It requires assessing your financial situation, health, family longevity, retirement lifestyle, and other sources of retirement income. While delaying CPP will increase your monthly payment, kicking it off earlier provides cash flow for a longer duration.

It may make sense to take your CPP retirement pension before age 65 if:

- You have insufficient income to cover your retirement living expenses. The early pension provides a cash flow bridge.

- You are no longer working, or you have minimal employment income, in your early 60s.

- You are in poor health and do not expect a long lifespan in retirement.

On the other hand, you may want to delay starting your CPP retirement pension past 65 if:

- You are still working full-time and earning a good salary.

- You have other sufficient sources of retirement income before age 65, such as a workplace pension.

- You are in good health and expect a long lifespan

- You want to maximize your CPP payments to provide a larger retirement income in later years.

What Happens If I Work While Receiving the CPP Retirement Pension?

If you continue to work while receiving your pension, you can increase your future payments through the CPP Post-Retirement Benefit (PRB). Your contribution obligation changes depending on whether you are under 65, between 65 and 70, or over 70.

- If you are under 65, you must still make the required CPP contributions on any employment or self-employment income you earn.

- If you are between 65 and 70, CPP contributions are optional. However, opting out is not automatic. You must file Form CPT30 with the CRA and provide a copy to your employer to stop contributions.

- After age 70, you no longer make or receive CPP contributions.

The PRB allows you to grow your CPP retirement pension further by continuing to contribute to the plan while working during your retirement years.

Is the CPP Retirement Pension Taxable?

The CPP retirement pension is taxable income. Unlike payroll income, income tax is not automatically withheld from your CPP payments. Understanding how CPP is reported on a tax slip, how it interacts with credits and other benefits, and how it fits into your broader tax picture is essential before your first payment arrives.

Keep these three regulatory realities in mind:

- Each year, you will receive a T4A(P) tax slip from Service Canada showing the total CPP income you received, which you must report on your tax return using CRA’s line 11400 instructions.

- CPP income is not eligible for the federal pension income tax credit. However, income from a workplace pension plan (RPP) or a Registered Retirement Income Fund (RRIF) is eligible.

- You and your spouse or common-law partner can apply to share your CPP retirement pensions. This can lead to tax savings if one partner is in a higher tax bracket.

CPP benefits do not qualify for the federal pension income amount (line 31400). If you want tax-planning options, CPP pension sharing (Service Canada) may reduce household tax in some cases, but it’s different from CRA “pension income splitting.”

Always consult a tax professional to determine whether pension sharing or voluntary tax withholding is the right move for your specific bracket.

FAQs about CPP Retirement Pension

[rank_math_rich_snippet id=”s-bb46bdcb-b5bd-4188-a4ca-cf58326b1e23″]

The Canada Pension Plan provides Canadian workers a solid foundation for retirement income security. Apply for your CPP up to 12 months before you want payments to start so your retirement cash flow begins as soon as you finish working. With proper planning and awareness of the CPP program, you can receive the full retirement pension that you contributed to and depend on a steady retirement income for your golden years.