Co-insurance is a cost-sharing arrangement commonly found in Canadian group benefit plans. In contrast, a co-pay is a fixed dollar amount that employees pay each time they use a specific covered service or product, regardless of the total cost. It results in different financial outcomes for both employers and employees.

This co-insurance vs co-pay difference influences how employees view costs when seeking care and how predictable their day-to-day expenses feel. Moreover, not all small businesses will benefit from the same cost-sharing model. Nonetheless, choosing the right benefits plan involves looking beyond just the initial costs. You need to consider what employees will actually pay based on real-life claims.

This article will compare co-insurance vs co-pays, which model is better, and how small businesses set up the best plan design.

What is Co-insurance in a Canadian Group Benefit Plan?

Coinsurance is the percentage of an eligible expense that the employee pays after satisfying any deductible, with the plan covering the remainder. The employer sets a coinsurance level, which determines how much the plan reimburses and how much the employee must pay out of pocket.

Co-insurance applies only after the employee has fulfilled any deductible required by the plan. Once that’s done, each eligible claim for the remainder of that plan year is subject to the co-insurance split. The employee is responsible for paying their set percentage (e.g., 20%) on every claim they submit.

What is a Co-pay in a Canadian Group Benefit Plan?

A co-pay is a fixed dollar amount that an employee pays out of pocket each time they access a covered product or service under their group benefit plan. That means the expense remains the same regardless of the overall expense.

Co-pays may be required for all products and services, only for certain products and services, or until the deductible has been met. This flexibility allows plan sponsors to apply co-pays selectively across different benefit categories.

How Co-Insurance and Co-Pays Differ in Canadian Small Business Benefit Plans

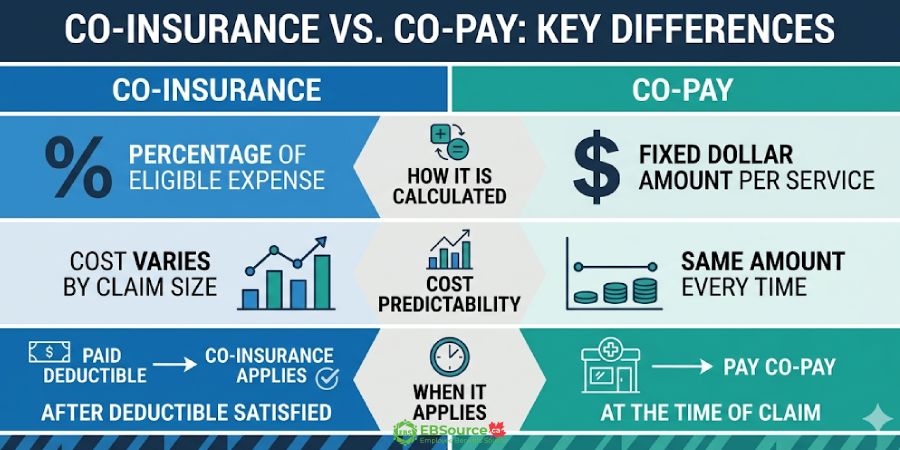

As can be seen from the definition, co-insurance is calculated as a percentage of eligible expenses, whereas a co-pay is a fixed dollar amount that must be paid for each service, regardless of the total charge. Another point to consider is that co-insurance generally applies after the employee has met their deductible; in contrast, a co-pay may be required for all products or services, for certain products or services, or until the deductible is met, depending on the plan design.

As a result, co-insurance and co-payments affect out-of-pocket costs differently, depending on the size of the claim. Additionally, the duration of the claims process varies based on the type of payout. Understanding these key differences enables both employers and employees to evaluate which option best suits their plan design and financial expectations.

The table below highlights the main structural differences between co-insurance and co-pay in a group benefit plan.

| Feature | Co-Insurance | Co-Pay |

| How it is calculated | Percentage of eligible expense | Fixed dollar amount per service or product |

| Cost predictability for employee | Varies with claim size | Same amount each time |

| When it applies | After the deductible is satisfied | At the time of claim (may apply before or after deductible, depending on plan) |

Is Co-Insurance or Co-Pays Suitable for Small Business Health Plans?

The best plan design option depends on the specific benefit category, the employee population’s usage patterns, and the employer’s willingness to accept cost variability. Among these, employee cost predictability is a significant factor for employers when choosing between copay and coinsurance models. However, both are valid components of a Canadian group benefits plan and can coexist within the same plan across various employee benefit categories.

With a co-pay, an employee filling multiple prescriptions each month knows the exact cost of each refill, regardless of changes in drug prices. In contrast, under co-insurance, the employee’s share fluctuates with the underlying cost of the service or product.

For low-cost, high-frequency claims like prescription refills, a flat co-pay makes employee benefits budgeting simpler. Regardless, for higher-cost, less frequent services such as major dental work, co-insurance allows both the employer and the employee to share the costs in proportion to their contributions. This way, neither party bears an unfair burden when dealing with large claims.

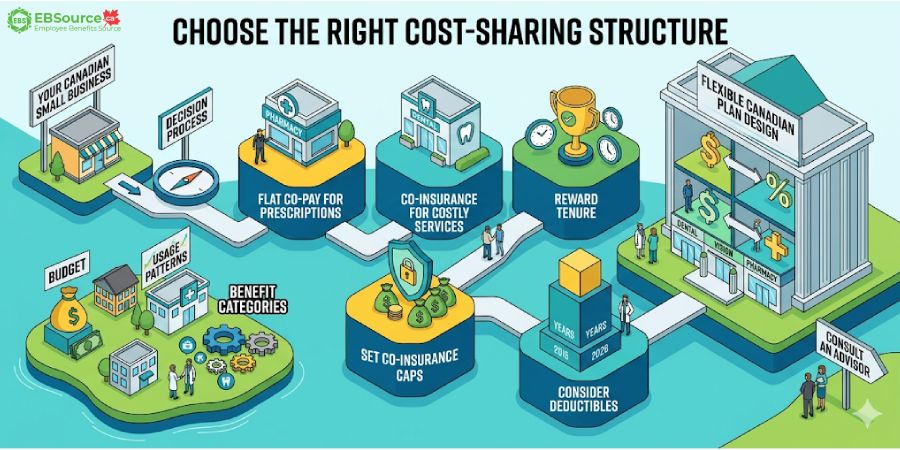

How to Choose the Right Cost-Sharing Structure for Your Small Business Benefit Plan

The suitable structure for your Canadian small business plans relies on the employer’s budget, the anticipated usage patterns of the employee population, and the benefit categories. While there is no one-size-fits-all answer, you can make a more informed decision by following five practical guidelines, which include using flat co-pays for prescriptions, co-insurance for costly services, setting co-insurance caps for budget control, offering rewards for long-term employees, and considering using deductibles.

The following considerations apply to most Canadian small business plan designs:

- Flat Co-Pay for Prescriptions: If employees frequently fill prescriptions, implementing a flat co-pay can simplify their budgeting and reduce confusion at the pharmacy.

- Co-Insurance for High-Cost Categories: When covering high-cost categories like major dental services, co-insurance shares the risk proportionally between the plan and the employee.

- Budget Predictability with Co-Insurance Caps: If budget predictability is a priority, co-insurance can help cap the employer’s exposure at a fixed percentage for each claim.

- Rewarding Tenure or Seniority: If the employer wants to reward tenure or seniority, co-insurance levels can be adjusted based on different employee groups.

- Common Approach with Deductibles: When a plan already includes a deductible, layering co-insurance on top is a common practice in Canada.

In practice, many Canadian group benefit plans default to co-insurance across most benefit categories, with a flat co-pay only where appropriate, such as for prescription drugs. Employers are not limited to one model; some insurers may offer plans that include a co-pay, while others might provide co-insurance instead, or even a combination of both. The flexibility to mix models across different benefit categories is one of the advantages of Canadian group plan design.

Before finalizing any cost-sharing structure, employers should consult a licensed benefits advisor who can model the projected cost impact for their specific employee population and claims history. Additionally, a Health Spending Account can serve as a useful cost-containment tool, providing employees with a capped annual amount to cover out-of-pocket expenses.

How Co-Pays and Co-Insurance Impact Employer and Employee Costs

Co-insurance links how much an employee pays to the claim amount, while a co-pay is a fixed fee for each use, making costs more predictable for the employee. The impact of each option varies for employers creating the plan and employees using it.

Below is an explanation of how these models impact the costs for both employees and employers:

How Each Model Affects Employers’ Costs

From the employer’s perspective, co-insurance is a useful way to control costs. Since the plan only pays a percentage of each eligible claim, the employer’s financial risk changes based on the claim amounts instead of facing large, unexpected payouts. This setup helps manage renewal premiums better because the plan does not have to cover all the costs of any single claim.

In contrast, a flat co-pay means employees pay a fixed amount for services or products, regardless of how much they cost. So, if the price of a prescription goes up, the employee still pays the same fee, and the plan covers the extra cost. This can lead to higher premiums over time, especially for services with rising costs. Nevertheless, sharing costs with employees helps keep the plan sustainable in the long run.

How Each Model Affects Employees’ Costs

From an employee’s perspective, make it easy for employees to budget because they know exactly what they will pay for each prescription refill. On the other hand, co-insurance can lead to different costs for every claim.

Therefore, employees who rarely use expensive services might like co-insurance, as it can keep their overall spending lower. However, those who often use cheaper services may prefer the predictability of co-pays.

Both models do more than just share costs; they motivate employees to be more conscious of their benefits usage. When employees chip in, they become smarter consumers, which reduces unnecessary spending and keeps the plan affordable for everyone. Whether their contribution is a percentage or a fixed amount, it encourages them to think about whether they really need a service or product before making a claim.